Empowering Women Through Government Initiatives

- Quick Summary

- What: Overview of top government schemes for women’s entrepreneurship in India.

- Why: To help women access financial resources, develop skills, and start or grow businesses.

- Who: Women entrepreneurs, aspiring business owners, and self-employed women.

- How: By leveraging government-backed loans, grants, and support platforms.

- Use Case: Helps women understand available funding schemes and select the most suitable option for their business or self-employment goals.

Empowering women is empowering the nation. In India, multiple initiatives have been launched to address the challenges women entrepreneurs face and ensure equal opportunities. Government schemes for women provide financial support, training, and mentorship to help women start or grow their businesses.

By accessing these schemes, women can secure funding for business setup, working capital, equipment purchase, or skill development, enabling them to stand firm on their entrepreneurial journey. Below, we cover the top 7 government schemes designed to empower women in India.

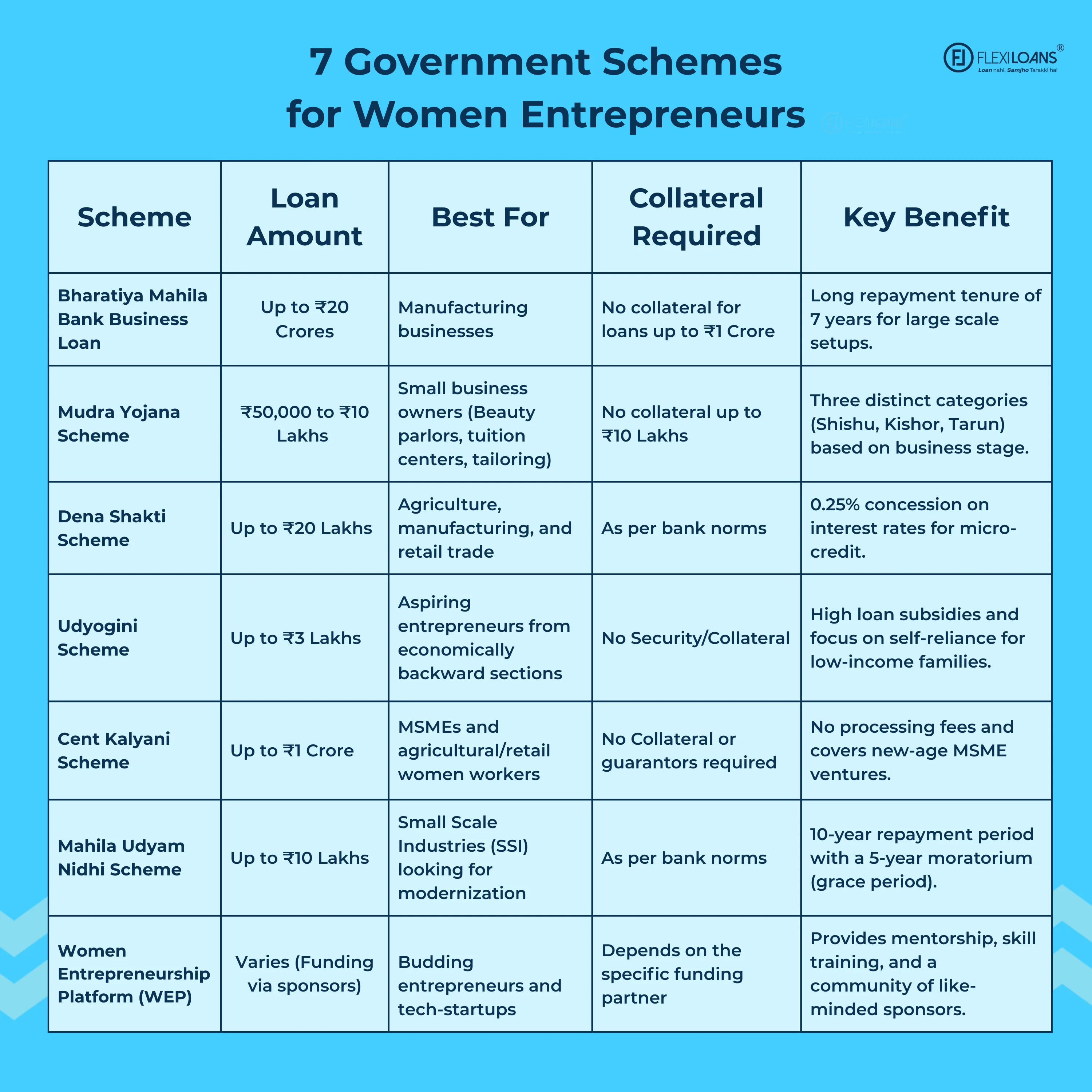

1. Bharatiya Mahila Bank Business Loan

This scheme supports women with limited resources who want to start a business. Women can borrow up to ₹20 crores, with a repayment period of 7 years. For loans up to ₹1 crore, no collateral is required under the Credit Guarantee Fund Trust for Micro and Small Enterprises.

Interest Rate: 10.25% + 2% extra = 12.25%

Use Cases: Manufacturing businesses, small retail shops, or local service enterprises.

Success Story: Nirmala Devi set up a shop in her village with a ₹25,000 loan, while another woman in Gujarat borrowed ₹5 lakh to create chocolate bouquets.

2. Mudra Yojana Scheme

The Mudra Loan empowers women small business owners and entrepreneurs. Loan limits are divided into three categories:

- Shishu: Up to ₹50,000

- Kishor: ₹50,001 – ₹5 lakh

- Tarun: ₹5 lakh – ₹10 lakh

Use Cases: Beauty parlors, tuition centers, tailoring units, and other small enterprises. Collateral is required only for loans above ₹10 lakh.

3. Dena Shakti Scheme

Dena Shakti scheme, designed for women in agriculture, manufacturing, micro-credit, retail, and other sectors:

- Micro-credit loans up to ₹50,000 with 0.25% interest concession

- For education, housing, and retail trading, loans up to ₹20 lakh

Provider: Dena Bank (visit nearest branch)

4. Udyogini Scheme

This Udyogini scheme targets women from low-income families (earning < ₹1.5 lakh/year) who wish to start a business without collateral.

- Loan Limit: Up to ₹3 lakh

- Interest Rate: Low, subsidized

- Use Cases: Any small business setup, particularly in economically backward communities

Goal: Promote self-reliance and financial independence.

5. Cent Kalyani Scheme

Launched by the Central Bank of India, this scheme benefits women who manage MSMEs or are starting new businesses.

- Loan Limit: Up to ₹1 crore without collateral

- Exclusions: Self-help groups, retail trade, educational institutions

- Key Benefits: No processing fee; market-linked interest rate

Use Cases: MSMEs, agricultural work, retail trading

6. Mahila Udyam Nidhi Scheme

Targeted at Small and Medium Enterprises (SMEs), this scheme is introduced by Punjab National Bank.

- Loan Limit: ₹10 lakh

- Repayment Tenure: 10 years (5-year moratorium included)

- Interest Rate: Market-linked

Goal: Modernize small-scale industries and provide technical and financial support to women entrepreneurs.

7. Women Entrepreneurship Platform (WEP)

WEP is a community platform for women entrepreneurs and sponsors to connect and collaborate.

- Services Offered:

- Incubation and acceleration programs

- Skill training and leadership mentorship

- Marketing and legal compliance support

- Funding and sponsorship connections

- Incubation and acceleration programs

Goal: Enable women to start businesses confidently while gaining mentorship and networking support.

Conclusion

These government schemes make women self-reliant and financially independent. The aim is to eradicate gender bias in entrepreneurship, provide equal access to business opportunities, and promote self-employment. Women can combine these initiatives with skill development, networking, and modern digital tools to maximize business success.

Alongside these business schemes, the Constitution and other initiatives support women’s education, rights, and equality across sectors. Other notable schemes include Ujjawala, Rajiv Gandhi National Creche Scheme, Priyadarshini, and Rashtriya Mahila Kosh (RMK).

By exploring these funding options and platforms, women can confidently set up businesses, access mentorship, and create sustainable income sources.

FAQs: Government Schemes for Women in India

Ans: Mudra Shishu loans or Udyogini Scheme are ideal for low-investment startups.

Ans: Bharatiya Mahila Bank Business Loan offers up to ₹20 crores, suitable for large-scale ventures.

Ans: Not for small loans (up to ₹1 crore in some schemes, such as Cent Kalyani or Bharatiya Mahila Bank).

Ans: Yes. WEP and other platforms offer mentorship, training, and networking opportunities.

Ans: Applicants can visit the respective bank branch or apply online through official portals for government loans.

Glossary: Key Terms Explained

| Term | Definition |

| MSME | Micro, Small & Medium Enterprises |

| Collateral-Free Loan | A loan that doesn’t require a property or asset pledge |

| Moratorium Period | The period during which repayment is paused after loan sanction |

| Incubation Program | Business support program providing mentorship, resources, and training |

| Entrepreneurship Platform | A community or network for business owners to connect and grow |