A complete guide on how self-employed professionals can access business loans for working capital, practice upgrades, and growth

Authored by FlexiLoans | Date: 06/02/2026

- Quick Summary

- What: Business loans for self-employed professionals are collateral-free funding solutions designed for doctors, chartered accountants, consultants, and other independent practitioners.

- Why: These loans help manage working capital needs, upgrade equipment, hire staff, and expand operations without pledging assets.

- Who: Professionals running clinics, CA firms, consulting practices, or advisory businesses.

- How: Digital lenders like FlexiLoans assess turnover, banking history, and credit profile to offer fast online approvals and disbursal.

- Use Case: A CA firm secures a business loan to hire temporary staff and invest in compliance tools before tax season, ensuring smooth operations without cash flow stress.

Running a professional practice goes beyond delivering services. Doctors need to maintain clinic infrastructure, accountants manage seasonal client surges, and consultants invest continuously in tools, talent, and marketing.

However, many self-employed professionals face difficulty accessing timely funding through traditional banks due to collateral requirements, strict eligibility rules, and lengthy documentation. A business loan for self-employed professionals solves this challenge by focusing on business performance and repayment capacity rather than fixed salaries.

This guide explains eligibility, documents, interest rates, and how professionals can apply for a business loan in India, along with why FlexiLoans is a preferred financing partner.

What Is a Business Loan for Self-Employed Professionals?

A Business loan for self-employed professionals is a collateral-free business loan designed for individuals operating independent practices. Approval is based on business turnover, bank statements, and creditworthiness rather than personal assets.

Common types include:

- Doctor practice loans for clinics, diagnostic centres, or nursing homes.

- CA firm financing for staffing, tax season workload, or software tools.

- Consultant business loans for operational growth, marketing, or technology upgrades.

- Professional practice loans for lawyers, architects, and advisory professionals.

Why Professionals Need Business Loans?

Self-employed professionals often experience fluctuating income cycles even when their practice is stable. A business loan helps bridge these gaps and support long-term growth.

1. Practice Setup or Expansion

Doctors and consultants can invest in new infrastructure, expand office space, or add new services.

2. Equipment and Technology Upgrades

Medical devices, diagnostic tools, accounting software, CRM tools, and automation platforms require high upfront costs.

3. Working Capital Support

Business loans help cover rent, salaries, vendor payments, and operational expenses during slow periods of revenue.

4. Hiring and Staffing Costs

CA firms often need additional staff during peak tax seasons, while clinics may require additional support staff.

5. Growth and Client Acquisition

Consultants and advisors may invest in branding, marketing, and business development tools to scale faster.

Key Benefits of Business Loans for Self-Employed Professionals

- Collateral-Free Funding: Borrow without risking personal or professional assets.

- Fast Disbursal: Funds are credited within 48–72 hours for urgent requirements.

- Flexible Loan Amounts: Borrow based on your business needs and financial profile.

- Minimal Documentation: Digital submission of essential financial documents.

- Multi-Purpose Usage: Funds can be used for equipment, salaries, rent, or working capital.

- EMI Structures Aligned to Cash Flow: Repayment schedules are tailored to your business revenue cycle.

Eligibility Criteria and Required Documents

Eligibility

To qualify for a business loan, professionals generally need:

- Minimum 1–2 years of professional practice.

- Monthly business turnover of ₹2 lakh or more.

- CIBIL score of 700 or higher.

- Indian citizenship, aged between 21 and 65.

- Registered professional practice or firm.

Required Documents

- PAN and Aadhaar cards.

- Professional qualification certificate (MBBS, CA, BDS, BAMS, or consultant credentials).

- Business or firm registration proof.

- Last 6–12 months’ bank statements.

- GST returns, if applicable.

- Additional financial documents as requested by the lender.

What are the Average Interest Rates for Professional Practice Loans?

| Lender Type | Typical Interest Rate (p.a.) | Ideal For |

| Public Banks | 11% – 15% | Established firms with strong credit history |

| Private Banks | 13% – 20% | Professionals with consistent turnover |

| NBFCs & Fintechs | 15% – 24% | Self-employed professionals needing fast approval |

At FlexiLoans, interest rates start at 1% per month and are evaluated based on turnover, credit profile, and cash flow.

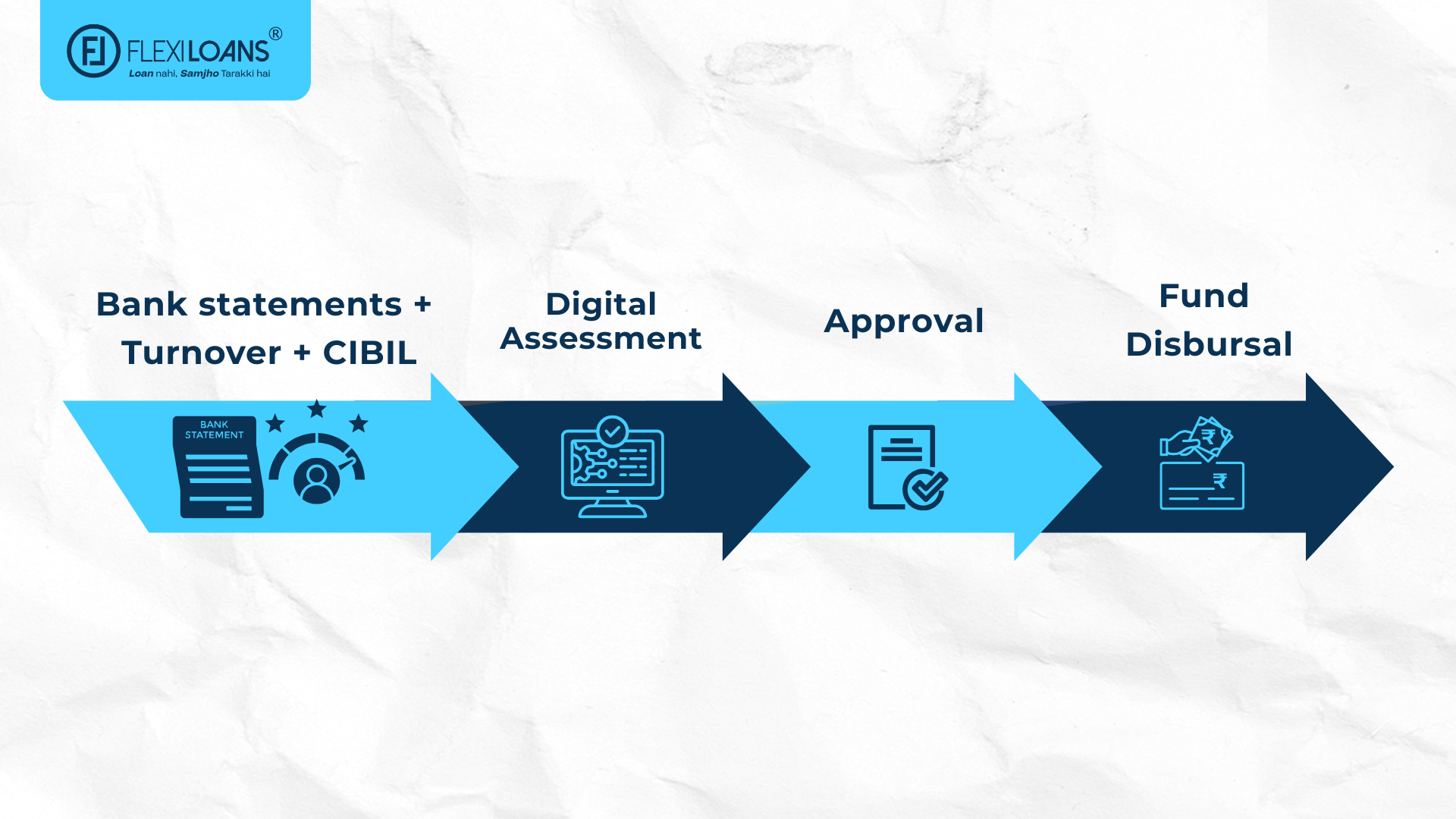

Application Process: How to Apply Online

- Assess Your Funding Needs – Determine whether the loan is for working capital, equipment, or expansion.

- Check Your Credit Score – A score above 700 improves approval chances and loan terms.

- Select a Lender – NBFCs like FlexiLoans provide faster processing and minimal documentation.

- Submit Online Application – Complete the form with professional and business details.

- Upload Documents – Submit PAN, Aadhaar, bank statements, and registration proofs digitally.

- Receive Approval and Disbursal – Approved loans are disbursed directly to your account promptly.

Why Choose FlexiLoans for Professional Financing?

FlexiLoans is a trusted digital NBFC, offering self-employed professionals tailored financing solutions:

- Rapid Approvals – Funds are typically disbursed within 48–72 hours.

- Collateral-Free Loans – Secure financing without pledging property or assets.

- Flexible Loan Amounts – Loans range from ₹50,000 to ₹50 lakh to meet diverse needs.

- Minimal Documentation – Digital KYC, bank statements, and registration proofs are sufficient.

- Transparent Pricing – No hidden fees; processing charges are clear upfront.

- Customised EMI Options – Repayment schedules align with business cash flows, reducing cash flow strain.

- Dedicated Professional Support – Expert guidance throughout the application process ensures smooth approvals.

Whether it is a doctor’s MSME loan, a consultant’s business loan, or CA firm financing, FlexiLoans provides a combination of speed, flexibility, and transparency that traditional banks often cannot match.

Pro Tips to Improve Approval Chances

- Maintain a CIBIL score above 700 to increase the likelihood of loan approval.

- Keep bank statements clear and consistent, reflecting regular revenue flows.

- Borrow only what your practice can comfortably repay to avoid unnecessary interest.

- Ensure all digital documents are up to date and accurate before submission.

- Compare loan tenure and EMI options to choose the most suitable plan.

- Maintain a strong business record, including professional registrations and compliance certificates.

Conclusion

Business loans for self-employed professionals help doctors, CAs, consultants, and other practitioners manage working capital, upgrade infrastructure, and scale operations efficiently. With digital lenders like FlexiLoans, professionals can access collateral-free funding with minimal documentation and faster processing compared to traditional banking routes.

FAQs: Business Loans for Self-Employed Professionals

Ans: It is a loan designed for professionals such as doctors, CAs, and consultants, where approval is based on turnover, bank statements, and credit profile rather than salary slips.

Ans: Any self-employed professional with a registered practice, a stable income stream, and at least 1–2 years of experience can apply.

Ans: Digital lenders like FlexiLoans can approve loans faster than traditional banks, depending on documentation and eligibility.

Ans: Yes. Loans can be used for clinic upgrades, software tools, hiring staff, marketing, and expansion.

Ans: No. FlexiLoans offers collateral-free business loans.

Ans: PAN, Aadhaar, bank statements, professional qualification proof, registration documents, and GST returns (if applicable).

Glossary: Key Terms Explained

| Term | Definition |

| Business Loan | A loan taken by a business to meet financial needs such as expansion, inventory, working capital, or operational expenses. |

| Professional Practice Loan | A business loan designed for self-employed professionals like doctors, CAs, consultants, lawyers, and architects to fund practice-related needs. |

| Self-Employed Professional | An individual who runs an independent practice or firm and earns income through services instead of a fixed monthly salary. |

| Working Capital | Funds are required to cover daily business operations, including salaries, rent, supplier payments, and utility expenses. |

| Collateral-Free Loan | A loan that does not require the borrower to pledge assets such as property, gold, or machinery as security. |

| Loan Eligibility | Lenders assess a borrower’s eligibility for a loan based on turnover, credit score, business age, and repayment capacity. |

| Credit Score (CIBIL Score) | A score ranging from 300 to 900 that reflects a borrower’s creditworthiness and repayment history. Higher scores improve loan approval chances. |

| Turnover | Total revenue generated by a business or practice during a specific period, usually monthly or annually. |

| Disbursal | The process of transferring the approved loan amount into the borrower’s bank account. |

| EMI (Equated Monthly Instalment) | A fixed monthly repayment amount that includes both principal and interest, paid until the loan is fully repaid. |

| Loan Tenure | The repayment duration of a loan is usually measured in months or years. |

| Interest Rate | The percentage charged by the lender on the borrowed amount, which determines the cost of the loan. |

| NBFC | A Non-Banking Financial Company that provides loans and financial services, often with faster digital processing than traditional banks. |

| Digital Lending | A loan process in which application, verification, approval, and disbursal are completed online with minimal paperwork. |

| Bank Statement | A financial record showing account transactions, used by lenders to evaluate cash flow and repayment capacity. |

| Practice Expansion | Business growth activities such as opening a new clinic/office, adding services, hiring staff, or upgrading infrastructure. |

| Invoice Financing | A funding option where businesses receive money against pending customer invoices to maintain cash flow. |

| Processing Fee | A one-time fee charged by the lender for loan application processing, documentation, and verification. |