A complete guide to how Udyam Registration strengthens MSME loan eligibility and improves approval chances.

Authored by FlexiLoans | Date: 23/12/2025

- Quick Summary

- What: Udyam Registration is the official government recognition for Micro, Small, and Medium Enterprises in India.

- Why: It allows MSMEs to access collateral-free loans, government-backed schemes, lower interest rates, and priority lending benefits.

- Who: Business owners, traders, manufacturers, service providers, and professionals applying for MSME loans in 2026.

- How: Learn how Udyam Registration works, how it supports loan approval, and why lenders prefer MSMEs registered under Udyam.

- Use Case: A small manufacturer increases the probability of loan approval and qualifies for CGTMSE-backed funding after completing Udyam Registration.

Udyam Registration has become one of the most essential steps for MSMEs applying for business loans in India. Whether you are a retailer, manufacturer, consultant, or medical professional, Udyam Registration gives your business an official identity under the Ministry of MSME.

For lenders, especially NBFCs and digital-first platforms, Udyam Registration acts as a reliable verification document. It confirms that the business is genuine, operational, and eligible for priority lending. In 2026, Udyam-registered businesses enjoy faster loan approvals, access to collateral-free credit, and eligibility for several government-backed schemes.

This guide explains the top benefits of Udyam Registration for MSME loan applicants, the link between registration and credit access, and how it enhances your probability of securing a business loan.

What Is Udyam Registration?

Udyam Registration is the government-issued certificate that officially recognises a business as an MSME. It is mandatory for businesses seeking benefits such as:

- Priority lending.

- Collateral-free loans.

- Subsidies and incentives.

- Government procurement advantages.

- Lower interest rate schemes.

Once registered, the business receives a unique Udyam Registration Number (URN) and a digitally verifiable certificate issued by the Ministry of MSME.

Why Udyam Registration Matters for MSME Loans?

Lenders prefer Udyam-registered businesses because registration verifies:

- The business category (Micro/Small/Medium).

- Legal existence of the enterprise.

- Financial behaviour (via PAN-linked data).

- Business activity type (manufacturing/service).

Without Udyam Registration, lenders must conduct additional checks, which can slow down or affect loan approval.

For MSME loan applicants in 2026, Udyam Registration significantly enhances trust and reduces lenders’ documentation burden.

What are the Key Benefits of Udyam Registration for Loan Applicants?

1. Access to Collateral-Free Loans (CGTMSE)

Udyam Registration makes MSMEs eligible for the Credit Guarantee Fund Trust for Micro and Small Enterprises. This allows businesses to secure collateral-free loans up to ₹5 crore under government-backed guarantees.

2. Higher Loan Approval Rates

Lenders prefer dealing with verified MSMEs. Udyam Registration indicates business authenticity and reduces the perceived risk for lenders, improving approval chances.

3. Eligibility for Lower Interest Schemes

Udyam-registered MSMEs may qualify for:

- Interest subvention schemes.

- Priority sector lending.

- Government-sponsored credit programmes.

4. Faster Loan Processing

With Udyam Registration, lenders require fewer supporting documents for verification. This results in quicker assessment and faster disbursal.

5. Recognition as a Formal Enterprise

Registration helps MSMEs build stronger financial credibility, useful for:

- Loan renewals.

- Higher loan amounts.

- Trade credit and vendor relationships.

6. Access to Government Tenders

Many public-sector tenders are available only to MSMEs. Udyam Registration enables access to procurement opportunities that support growth.

7. Trusted Compliance Status

Udyam-registered MSMEs are seen as compliant, valid enterprises, an essential factor for NBFCs, banks, and fintech lenders.

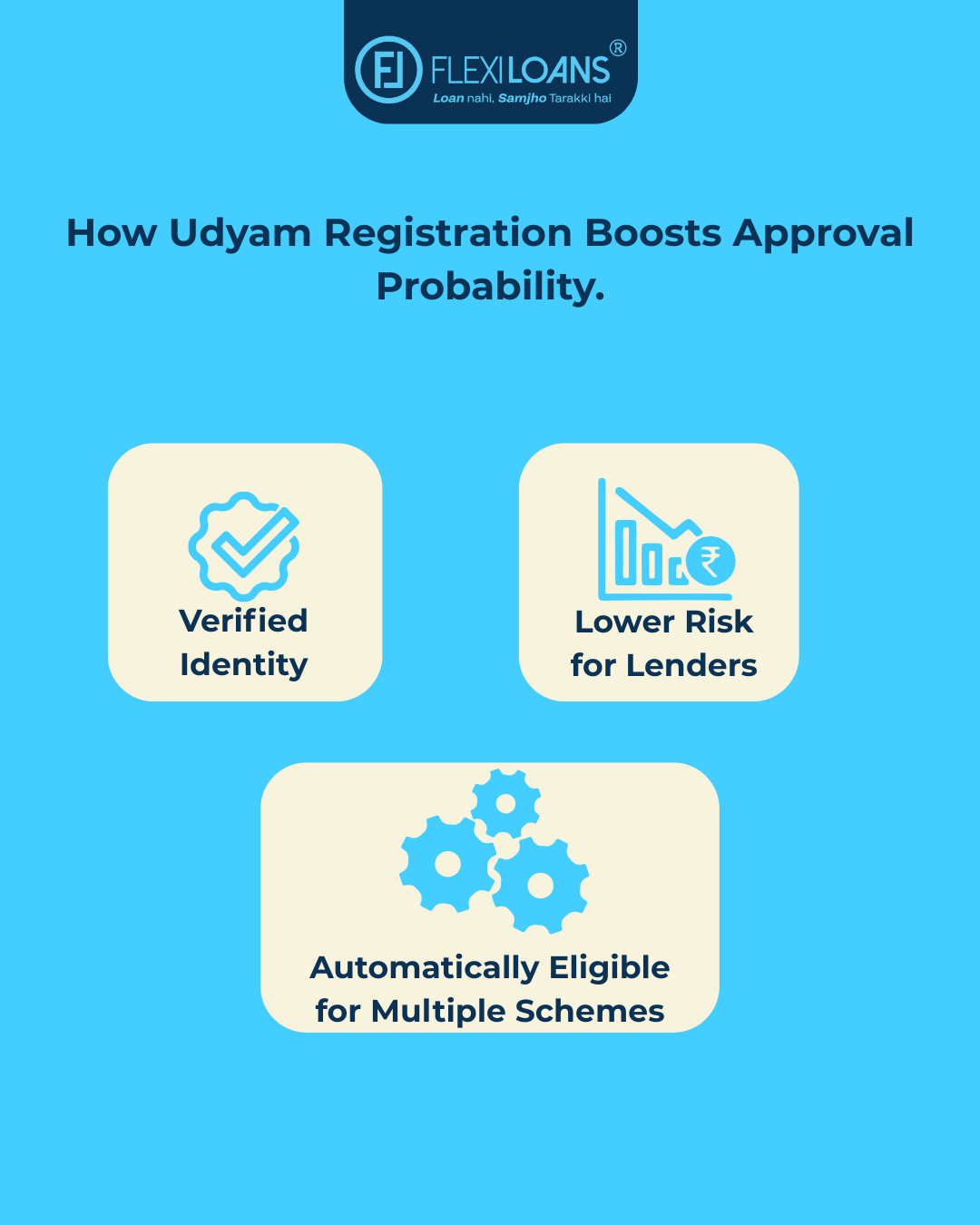

How Udyam Registration Improves Loan Approval Odds?

Udyam Registration strengthens loan applications in 3 significant ways:

1. Verified Identity

It proves the business is active, legal, and meets MSME criteria.

2. Lower Risk for Lenders

Lenders are more confident in granting loans to formalised MSMEs with transparent records.

3. Automatically Eligible for Multiple Schemes

Schemes like CGTMSE reduce lenders’ risk, increasing the likelihood of approval for borrowers.

Eligibility: Who Should Register on the Udyam Portal?

Businesses that should register under Udyam include:

- Retail shops.

- Traders.

- Micro and small manufacturers.

- Service-based professionals.

- Medical practices.

- Consultants and freelancers.

- Digital service businesses.

Any enterprise meeting the MSME investment or turnover thresholds should register.

What Documents are Required for Udyam Registration in 2026?

- Aadhaar number of the business owner.

- PAN of an individual or entity.

- Business bank account details.

- Basic business information (activity, NIC code, turnover).

No physical documents are needed; everything is validated online.

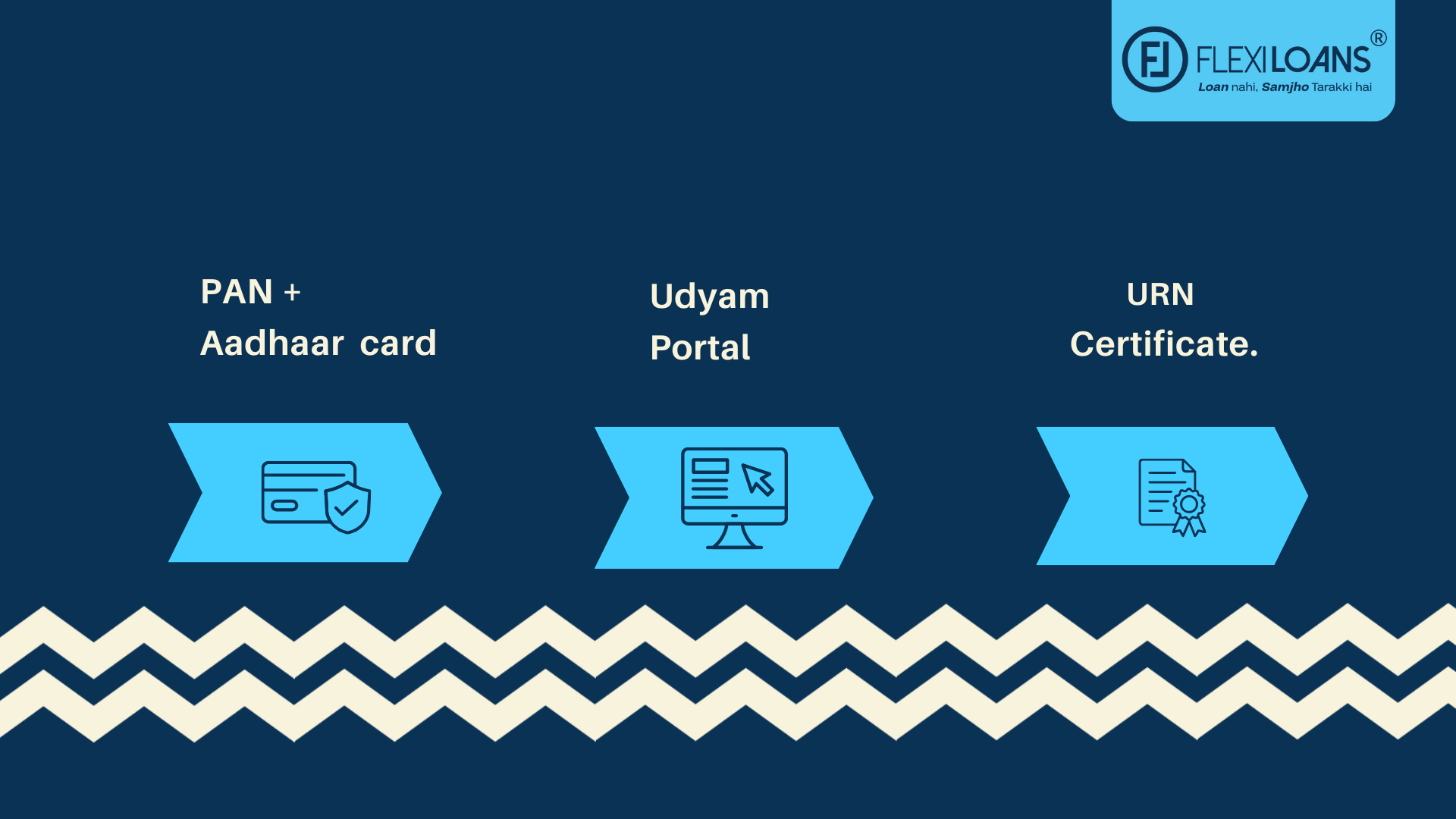

What is the Latest Udyam Registration Process to be followed in 2026?

Udyam Registration is entirely paperless and completed in minutes.

Step 1: Visit udyamregistration.gov.in

Step 2: Enter Aadhaar + PAN details

Step 3: Provide business information

Step 4: Validate OTP

Step 5: Receive Udyam Registration Number (URN)

Your digitally verifiable Udyam certificate is generated instantly.

Why Choose FlexiLoans for Your MSME Loan?

FlexiLoans is trusted by thousands of business owners across India. For medical professionals, we offer:

- Fast loan disbursal within 48–72 hours.

- Minimal documentation and 100% digital processing.

- Collateral-free MSME loans tailored to clinic needs.

- Transparent charges with zero hidden fees.

- Loan amounts ranging from ₹50,000 to ₹50 lakh.

- EMIs are designed around clinic cash flow patterns

What are the Pro Tips to Improve Your MSME Loan Approval?

- Maintain a CIBIL Score Above 700 for better chances of approval.

- Borrow Only What You Need to avoid unnecessary interest.

- Keep Digital Documents Ready, especially bank statements and GST filings.

- Compare Tenure and EMI Options before finalising the loan.

- Provide Accurate Information to avoid delays or rejection.

In 2026, Udyam Registration has become a critical requirement for MSMEs seeking timely access to credit. It enhances transparency for lenders and simplifies the entire loan approval process.

Conclusion

Udyam Registration is more than just a government certificate; it is a powerful enabler for MSMEs seeking collateral-free loans, better interest rates, and faster approvals. For business owners planning to apply for MSME loans in 2026, Udyam Registration is one of the most critical first steps.

With digital lenders like FlexiLoans, MSMEs can access funding quickly and confidently, supported by transparent, paperless processes that keep pace with today’s business environment.

FAQs: Udyam Registration for MSME Loans (2026)

Udyam Registration is the official government certification that identifies your enterprise as an MSME under the Ministry of MSME. It establishes your business as a formal entity, enabling access to financial benefits, credit support, and government schemes explicitly designed for small businesses.

It is not mandatory for every lender, but having a valid Udyam Registration significantly improves your chances of loan approval. Registered MSMEs are seen as more credible and eligible for collateral-free credit schemes, which makes the lending process smoother and faster.

Udyam Registration improves eligibility for collateral-free loans, speeds up verification, and opens access to government-backed schemes such as CGTMSE. It also helps MSMEs qualify for lower-cost credit programmes, interest support schemes, and priority lending benefits.

The process is entirely online and generally finished within a few minutes. Business owners simply provide their Aadhaar, PAN, and basic business details, and the Udyam Registration Number (URN) is issued instantly.

Physical documents are not needed. You only need Aadhaar, PAN, and key business information such as activity type and turnover. Since the portal verifies everything digitally, the process remains quick and paperless.

Glossary: Key Terms

| Term | Definition |

| Udyam Registration | Government certification officially recognising a business as an MSME. |

| Udyam Registration Number (URN) | A unique ID is issued to MSMEs after successful registration. |

| MSME | Micro, Small, and Medium Enterprises based on turnover and investment criteria. |

| MSME Loan | Business loan available to eligible micro, small, and medium enterprises. |

| Collateral-Free Loan | A loan granted without requiring the borrower to pledge property or assets. |

| CGTMSE | Government-backed Credit Guarantee Fund Trust provides guarantee cover for MSME loans. |

| Priority Sector Lending | Mandatory lending by banks to sectors such as MSMEs to support growth. |

| Interest Subvention | Government-supported interest rate relief offered to MSMEs. |

| Digital KYC | Paperless identity verification using Aadhaar and PAN. |

| Turnover | Total revenue generated by a business in a financial period. |

| Business Vintage | Number of years a business has been operational. |

| Fintech Lender | Digital-first financial institution offering quick, technology-driven loans. |

| Disbursal | Transfer of approved loan funds to the borrower’s bank account. |

| Working Capital | Funds used for daily operations such as salaries, inventory, and vendor payments. |

| Loan Tenure | The period over which the borrower repays the loan through EMIs. |