Understand RTGS in banking, a real-time fund transfer method ideal for high-value business transactions. Learn how it works, timings, charges & more.

Authored By FlexiLoans | Date: 08/09/2025

- Quick Summary

- What: RTGS is an instant fund transfer system used for high-value transactions (₹2 lakh and above).

- Why: It enables real-time settlement between banks, reducing delays, improving cash flow, and enhancing payment security.

- Who: Businesses, government bodies, and individuals who need to transfer large sums securely and without batch delays.

- How: Log into your bank’s net or mobile banking, enter beneficiary details, authorise the RTGS transfer, and the funds are instantly settled.

- Use Case: Businesses use RTGS for vendor payments, bulk salaries, or tax settlements; ideal for urgent and large-value transfers.

Introduction

Businesses and individuals require fast and secure methods for transferring funds. With the increasing demand for instant financial transactions, banks offer various digital payment methods. Among them, RTGS (Real-Time Gross Settlement) stands out as a trusted and efficient system for high-value transfers.

RTGS enables the immediate transfer of funds between banks without delays. Unlike NEFT, which processes payments in batches, RTGS settles each transaction instantly. This system is widely used by businesses, government bodies, and individuals who need to transfer ₹2 lakh or more.

The Reserve Bank of India (RBI) launched it to streamline financial transactions and ensure that large payments clear promptly. Companies rely on this for vendor payments, salary transfers, and bulk transactions, thereby reducing their reliance on cheques or demand drafts.

Similarly, FlexiLoans offers seamless financial support to businesses. Whether you need funds for working capital or expansion, access to flexible financing simplifies financial management. Discover how a Business Loan for Working Capital can help you manage your cash flow effectively.

RTGS Full Form & Meaning

What is RTGS?

It stands for Real-Time Gross Settlement. This system ensures that transactions occur instantly and individually, without batch processing. Banks settle payments immediately, allowing recipients to access funds promptly without delay.

RTGS Meaning in Banking

- Transactions settle one at a time, ensuring real-time processing.

- Funds move directly from the sender’s account to the recipient’s without waiting for scheduled settlements.

- RTGS is best suited for large-value payments, providing a secure and efficient banking solution.

How RTGS Differs from Other Fund Transfer Methods

Many businesses and individuals often compare RTGS with other fund transfer methods, such as NEFT and IMPS. While all three systems facilitate digital transactions, they operate differently in terms of speed, settlement type, and transaction limits.

- RTGS vs NEFT: NEFT settles payments in batches at fixed intervals, which can lead to delays. In contrast, RTGS completes each transaction instantly.

- RTGS vs IMPS: IMPS allows immediate transfers but has an upper limit of ₹5 lakh per transaction. RTGS, however, handles much larger payments without any cap, making it more suitable for high-value transactions.

For example, if a company needs to pay ₹10 lakh to a supplier, RTGS ensures instant fund settlement, whereas IMPS would require multiple transfers.

Step-by-Step RTGS Transfer Process

Making an RTGS transfer is simple. Follow these steps:

- Log in to your banking platform – access net banking, mobile banking, or visit a branch in person.

- Select the RTGS transfer option – locate it under the Fund Transfer section.

- Enter recipient details – Provide:

- Beneficiary’s full name

- Bank account number

- IFSC code of the recipient’s bank

- Amount to transfer

- Authorise the transaction – Use an OTP or security PIN for authentication.

- Funds settle instantly – The bank deducts the amount from your account and credits it to the recipient.

Minimum & Maximum Transfer Limits

- Minimum RTGS transaction: ₹2 lakh

- Maximum transaction: No upper limit (depends on the bank).

For businesses managing high-value transactions, RTGS offers a secure and efficient alternative to traditional fund transfers. Similarly, FlexiLoans provides instant financial solutions, ensuring companies never face cash flow challenges.

RTGS Timings & Working Hours

Availability

Since December 2020, RTGS has operated 24/7, including weekends and bank holidays. This round-the-clock availability ensures businesses and individuals can make urgent transactions whenever needed.

Bank Working Hours

- Online banking – Available anytime, ensuring seamless digital transfers.

- Branch-based RTGS – Availability depends on the bank’s working hours; typically available during business days.

RTGS Processing Time

- Most RTGS transactions settle within 30 minutes. If a system issue delays the transaction, banks typically refund the amount on the same day.

Businesses depend on efficient cash flow management. RTGS facilitates instant high-value transfers, while FlexiLoans offers Invoice Financing to help companies maintain liquidity without disrupting daily operations.

RTGS Charges & Fees

- Online RTGS Transfers (Net Banking / Mobile Banking)

No Charges (as per RBI guidelines).

- RTGS Transfer via Bank Branch

Transaction Charges (as per RBI regulations):

- ₹2 lakh – ₹5 lakh: Up to ₹25 per transaction.

- Above ₹5 lakh: Up to ₹50 per transaction.

Some banks charge additional fees for branch-based RTGS transactions, making online transfers a more cost-effective option.

RTGS transformed high-value fund transfers in India by making them instant, secure, and seamless. For MSMEs, this isn’t just a convenience; it’s a lifeline for managing vendor payments, salaries, and working capital efficiently.

RTGS Charges Compared to NEFT & IMPS

| Transfer Method | Charges (Online) | Charges (Branch) | Best Use Case |

| RTGS | Free | ₹25 – ₹50 | Large-value payments |

| NEFT | Free for individuals | Nominal charges for businesses | Small to medium transfers |

| IMPS | Bank-dependent | Bank-dependent | Instant small transactions |

Managing transaction costs effectively is crucial for businesses. Besides RTGS, businesses can also explore Government Loan Schemes to access affordable financing and reduce financial strain.

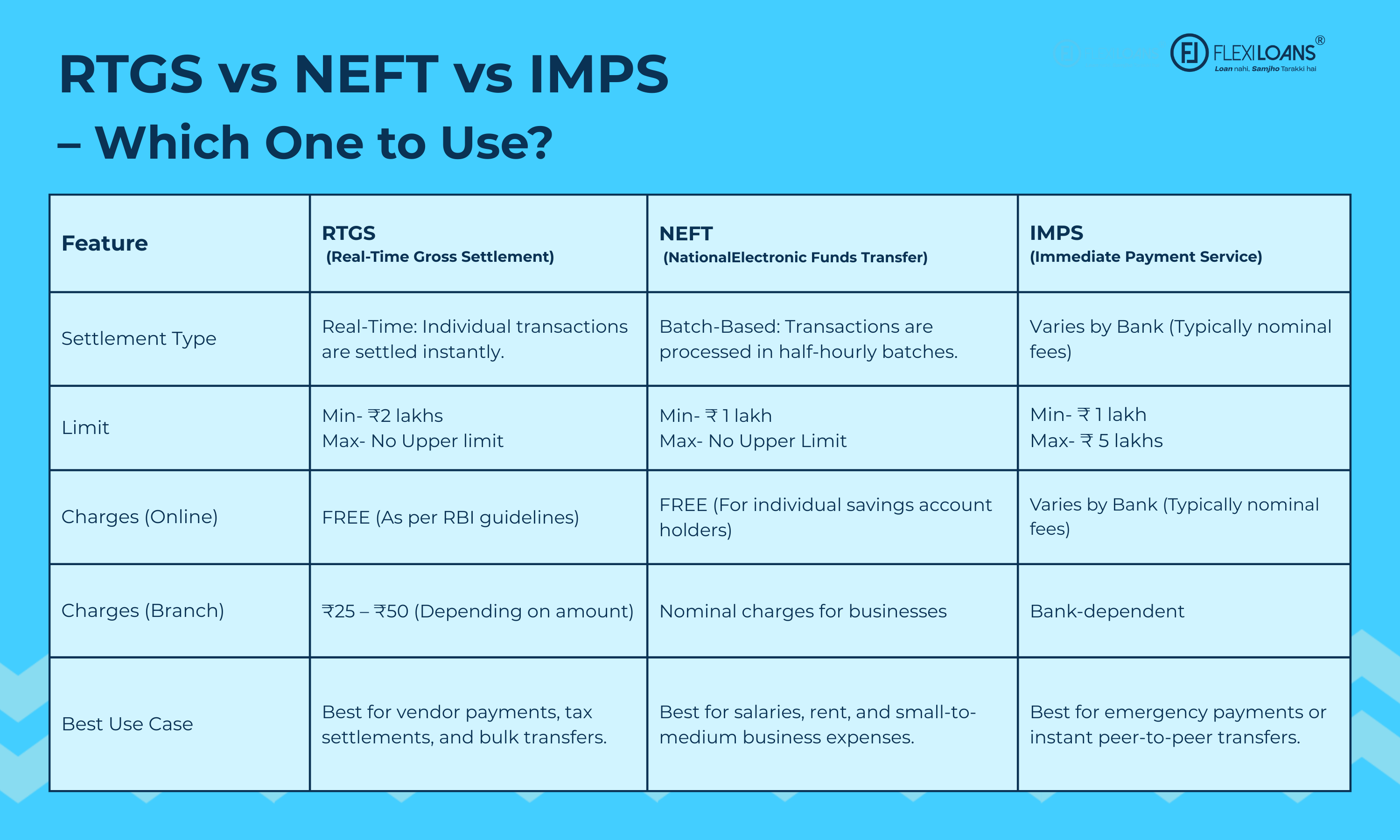

RTGS vs NEFT vs IMPS – Key Differences

| Feature | RTGS | NEFT | IMPS |

| Settlement Type | Real-time | Batch-based | Instant |

| Minimum Amount | ₹2 lakh | No minimum | ₹1 |

| Maximum Amount | No limit | No limit | ₹5 lakh |

| Timing | 24/7, 365 days | 24/7, 365 days | 24/7, 365 days |

| Charges | Free online, branch charges | Free for individuals | Varies by bank |

| Best For | High-value transfers | Small to medium transactions | Urgent small transfers |

RTGS, NEFT, and IMPS serve different purposes based on transaction value and urgency. RTGS processes real-time settlements for high-value transactions (₹2 lakh and above), with no upper limit, making it ideal for businesses. NEFT operates on a batch-based system, suitable for small to medium transfers with no minimum amount. IMPS, on the other hand, provides instant fund transfers but has a ₹5 lakh cap, making it best for urgent, small-value payments. While RTGS is free online but chargeable at branches, NEFT is usually free, and IMPS charges vary by bank.

When Should You Use RTGS?

- They are the best choice when transferring ₹2 lakh or more instantly. Since it operates on a real-time settlement system, funds are transferred to the recipient without delay. Businesses frequently use RTGS for supplier payments, bulk salary transfers, and high-value government transactions. If you run an MSME and need additional funding for business expansion, check out MSME Loans to boost growth and sustain operations.

When is NEFT Better?

- NEFT is ideal for small to medium transactions that do not require immediate processing. Since NEFT operates in a batch-based settlement system, funds may take some time to reach the recipient. It suits individuals and businesses that make routine payments where instant transfers are not necessary.

When Should You Choose IMPS?

- IMPS is ideal for making instant small transactions, particularly for urgent fund transfers of up to ₹5 lakh. It works like UPI, ensuring quick money transfers.

Businesses managing frequent high-value payments prefer RTGS, while those requiring additional funds for expansion rely on FlexiLoans for hassle-free financing.

What are the Benefits of RTGS?

✔ Instant Settlement – RTGS ensures real-time fund transfers without delays. Unlike NEFT, which operates in batches, it prevents delays, making it ideal for urgent high-value payments.

✔ Highly Secure – Since the Reserve Bank of India (RBI) regulates RTGS, it remains one of the safest electronic payment systems. The direct bank-to-bank transfer mechanism eliminates intermediaries, reducing fraud risks.

✔ Ideal for Large Payments – Companies use RTGS to pay vendors, manage supplier invoices, and settle financial obligations promptly.

✔ 24/7 Availability – Since December 2020, RTGS has been operating round the clock, including weekends and public holidays. Businesses and individuals can transfer funds at any time, without relying on banking hours.

✔ Zero Charges for Online RTGS – Digital transactions via net banking and mobile banking are entirely free, reducing transaction costs for businesses and individuals.

Limitations of RTGS

🔹 Minimum Transfer of ₹2 Lakh – RTGS is unsuitable for small transactions, as banks do not allow transfers below ₹2 lakh using this system. Individuals making lower-value payments prefer NEFT or IMPS.

🔹 Branch-Based RTGS Charges – While online RTGS is free, branch-based transactions incur charges. These range from ₹25 for transfers between ₹2 lakh and ₹5 lakh, and ₹50 for payments above ₹5 lakh.

For businesses, managing cash flow efficiently is crucial. While RTGS enables instant high-value transfers, companies often need additional working capital. This is where FlexiLoans offers quick business loans, ensuring enterprises have the necessary funds to operate and grow.

Conclusion

RTGS is a secure, fast, and reliable method for transferring high-value funds. With real-time settlement, 24/7 availability, and zero charges for online transactions, it remains a preferred option for businesses and individuals.

By using this alongside financial solutions from FlexiLoans, companies can manage cash flow efficiently, handle supplier payments, and expand operations without financial stress. If you need quick funds without collateral, explore Unsecured Business Loans to keep your business running smoothly.

FAQs

No, RTGS is designed explicitly for high-value transactions. The minimum transfer amount is ₹2 lakh, making it unsuitable for smaller payments. For lower-value transactions, NEFT or IMPS would be a more suitable option.

RTGS usually settles within minutes. In rare cases, it may take up to 30 minutes or be refunded the same day.

Online RTGS transfers via the net or mobile banking are free. However, branch-based RTGS may incur charges up to ₹50.

Yes, many banks allow you to schedule RTGS transactions in advance for a selected date.

Failed RTGS transactions are refunded within 24 hours. For persistent issues, contact your bank’s support.

RTGS stands for Real-Time Gross Settlement. It enables instant and individual settlement of high-value fund transfers without batch processing.

The full form of RTGS is Real-Time Gross Settlement, a payment system for the immediate settlement of large transactions.

The minimum amount for RTGS is ₹2 lakh. Transactions below this amount are not processed under RTGS.

Yes, since December 2020, RTGS has been available 24/7, including weekends and public holidays.

Yes, RTGS is regulated by the RBI and offers a highly secure mechanism for high-value business transfers.

RTGS is real-time and suited for large payments. NEFT is batch-based with no minimum limit, while IMPS is instant but capped at ₹5 lakh.

Glossary: Key Terms Explained

| Term | Definition |

| RTGS Full Form | RTGS stands for Real-Time Gross Settlement. |

| RTGS | A real-time settlement system used for transferring funds individually and immediately. |

| NEFT | National Electronic Funds Transfer settles transactions in batches rather than in real time. |

| IMPS | Immediate Payment Service allows instant transfers up to ₹5 lakh, commonly used for personal needs. |

| IFSC Code | A unique alphanumeric code identifying each bank branch, essential for processing electronic payments. |

| Transaction Limit | The minimum and maximum permissible amount per transaction in a fund transfer system. |

| OTP | One-Time Password used for authenticating digital banking transactions. |

| Settlement | The completion of a fund transfer from the sender to the recipient’s account. |

| Working Capital | The funds available to manage the day-to-day operations of a business. |